Let me start today’s article with an admission: Closed-end funds (CEFs) are my passion—but not only for their 8%+ dividends (often paid monthly).

The main reason I’ve been investing in these terrific high-yield vehicles for years is, in fact, very personal: Over a decade ago, CEFs’ high yields gave me enough passive income to quit my job.

I was a professor at the time, and I decided to quit to live on my income. As I started preaching the gospel of CEFs, more people heard the call, and my CEF Insider advisory, launched back in the spring of 2017, was born.

But I’ll also admit that I’ve flirted with other big-yielding options, and they all came up short. Take exchange-traded notes (ETNs), which came and went years ago. I quickly dipped into these only to get out just as fast: these are empty assets that don’t actually own anything, which is why I warned readers to avoid them seven years ago.

I also tried master limited partnerships (MLPs), then quickly discovered the tax-filing nightmare involved with them. (MLPs issue a K-1 package to report your income, which is a headache compared to the 1099 form you get from stocks).

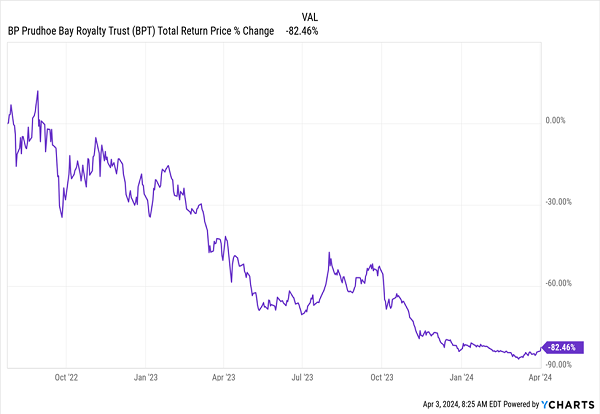

Similarly, royalty trusts were a bust; in July 2022, I warned about these and pointed to potential disaster with the BP Prudhoe Bay Royalty Trust (BPT). Here’s how BPT has done since then.

BPT Loses Most of Its Value

Another admission: This was a relatively easy call, as commodity stocks were generally near the bottom of asset classes in returns in the six years prior to 2021 and 2022 before soaring 38.5% and 22% in those years, respectively. That was overdone and set up a correction.

Truth is, an oil pipeline is hard to make money on for anyone but the people working on the pipeline. That means that both royalty trusts and MLPs, which focus on finding and transporting energy, are often poor investments in the long run (though they can be profitable if you time them right).

BDCs Take the Silver Medal—But Caution Is Key

That leads me to another high-yielding asset class (besides CEFs) that I continue to flirt with: business development companies, or BDCs.

The caveat here is that with BDCs—even more so than CEFs and other income plays—the quality of the assets (loans in this case), is critical. That’s because this is a complex area of the market where poor-quality investments are hit especially hard.

BDCs, put simply, collect investor money and lend it to mostly medium-sized businesses in the private credit market (these are companies that borrow from BDCs instead of banks). BDCs then send the interest on those loans back to investors.

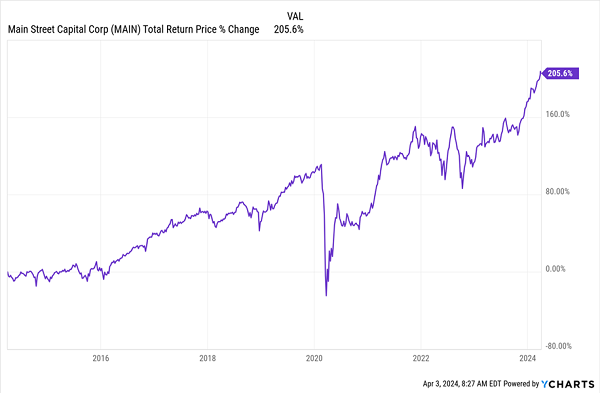

Some BDCs are great and have been for a long time. Consider Main Street Capital Corporation (MAIN), for instance:

MAIN Rides Its Big Dividend (and Gains) to a Triple-Digit Run

As you can see above, MAIN is a BDC success story, posting a relatively stable 206% total return over a decade, thanks to its smart lending practices. Its dividend (current yield: 6.1%) has also grown reliably, with some special payouts (the spikes in the chart below) thrown in over the years.

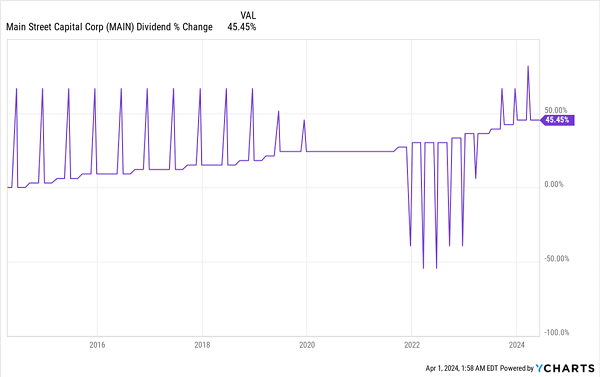

MAIN Boosts Dividends, Delivers Special Payouts, Too

This is a strange chart, and the pandemic is partly to blame for that. MAIN paused special payouts during that dark time. When they restarted in 2022, they were smaller than the BDC’s regular payout (unlike the huge special payouts that gave MAIN an annualized yield of over 8% for most of the late 2010s). That’s the reason for the downward-pointing spikes you see above.

However, those bigger payouts have recently restarted and could kick MAIN into higher-yielding territory for a long time to come.

Thus we see with MAIN, which is one of the best BDCs, the higher risk you’d expect with mid-sized businesses: in times of economic stress, loans to these firms will yield less because mid-sized firms are often hit harder than bigger ones.

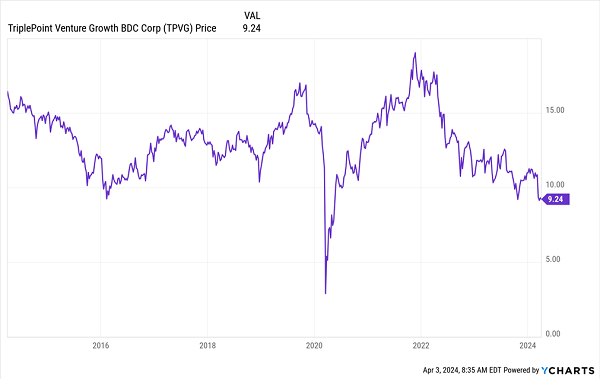

Credit quality is another complication with BDCs. Consider this chart for another BDC, the TriplePoint Venture Growth BDC Corp (TPVG).

TPVG’s Sliding Price

TPVG has paid a consistently high income stream, and its yield today is off the charts: 17.3%. However, its stock price has been falling consistently since late 2021, with no recovery. What’s going on here?

TPVG has seen its net asset value (NAV, or the value of the loans it holds) fall significantly, now around $9.21 a share, down from $14.01 at the end of 2021.

The reason why is simple: TPVG has had to downgrade many of its loans as mid-sized firms struggle. Its focus on tech didn’t help, as rising interest rates hit many small techs hard. There have also been more downgrades in valuations across BDCs.

Moreover, companies that borrow money from BDCs pledge their assets as collateral, and given that these are private firms, those assets are often difficult to value. In some cases, lenders have hired private investigators to help discern the value of the assets these firms are borrowing against.

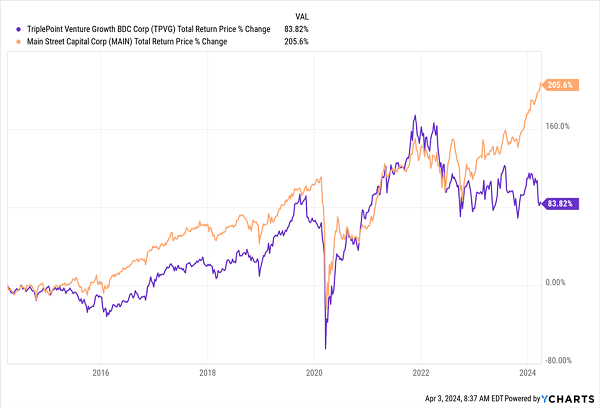

That, of course, adds risk. And it’s why these firms are only for those who can handle that type of risk, as poorly run BDCs can seriously weigh on your returns. Consider the stall we’ve seen with TPVG compared to MAIN:

TPVG Falls Off the Pace

TPVG was flying high with MAIN before the pandemic and rode the post-pandemic recovery, but a tough portfolio meant it couldn’t ride that recovery to new heights. If uncertainty about portfolio quality continues, more BDCs could follow TPVG and make a sudden, swift turn.

The last word on BDCs? If you can find the good-quality picks and avoid the bad ones, there’s a lot of good income to earn here. But doing so requires a lot more legwork and expertise than analyzing investments like stocks, ETFs and CEFs.

These “AI-Powered” 7.8% Payouts Will Crush BDCs (and Regular Stocks, Too)

Like I said, I’m flirting with BDCs. But because of the risks, and how hard it is to value their portfolios, I’m loath to recommend them now—especially when we’ve got plenty of stable, bargain-priced 8%+ dividends waiting for us among CEFs.

One of the advantages of CEFs is that they let us target our investments at specific sectors in a way that BDCs don’t.

Want to target large-cap equities? There are CEFs for that.

Healthcare stocks? There are CEFs for that, too.

Artificial intelligence stocks? Well, there are CEFs for that, too! In fact, I’ve compiled my top 4 CEFs for tapping the surging AI megatrend in a special “AI-Powered” portfolio that pays an outsized 7.8% now.

This unique CEF “mini-portfolio” is the only place you can still buy AI stocks for cheap—as these 4 funds ALL trade at deep discounts to net asset value (NAV).

I don’t expect that to last, though, as AI continues to supercharge US productivity, and “late to the party” investors desperately search for a way in.

We’ll be there well ahead of them!

Click here to learn more about these four 7.8%-yielding (and deep-discounted) “AI-Powered” funds and get a FREE Special Report naming each one.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Growth stocks offer a lot of bang for your buck, and we've got the next upcoming superstars to strongly consider for your portfolio.

Get This Free Report