From being nickel-and-dimed on fees to having loans called in and credit lines cut off during the 2008 financial meltdown, banks have come a long way in recovering regarding solvency, reputation and underlying stock prices. You may have missed the rally in bank stocks and have wondered, "When is a good time to invest?"

Interest rate hikes should be good for banks since they collect income from higher interest rates on deposits and loans, right? Banks continue to report huge profits, and you may want in on the action. Let's go over the basics of investing in bank stocks and how to invest in bank stocks so you can hit the ground running if you're looking for bank stocks to buy.

Key Takeaway

Investing in bank stocks involves purchasing shares of publicly traded banks to earn dividends and capital gains. Consider key metrics to evaluate the bank's performance and profitability. Diversifying your portfolio with bank stocks can provide stability and potential growth opportunities.

Introduction to Investing in Bank Stocks

The history of bank stocks is intertwined with the ebb and flow of financial markets. In the wake of the 2008 financial meltdown, banks faced a reckoning. Many faltered under the weight of their missteps, while others emerged stronger. Today, each institution tells its story through metrics like price-to-earnings ratio, return on equity and net interest margin.

Understanding the banking sector is not only about analyzing balance sheets and market trends. It’s a journey into economic dynamics, the global economic climate and regulatory frameworks.

Understanding Bank Stocks

Bank stocks represent ownership in financial institutions. As an investor, buying bank stocks gives you a claim on the bank's future profits. Let’s get to know the different types of bank stocks.

Commercial Banks

These large banks like Bank of America Co. NYSE: BAC, JP Morgan Chase NYSE: JPM and Wells Fargo & Company NYSE: WFC provide traditional services to retail customers and businesses. They make money by charging interest on loans and keeping some deposits as profit. Commercial banks thrive when interest rates are rising.

Regional Banks

Regional banks focus on consumers and businesses in specific geographic areas. Examples include The PNC Financial Services Group Inc. NYSE: PNC and U.S. Bancorp NYSE: USB. Regional banks can be a good investment if you believe a certain location will see economic growth.

Investment Banks

Institutions like The Goldman Sachs Group Inc. NYSE: GS and Morgan Stanley NYSE: MS work with governments, corporations and high-net-worth individuals. They provide services like underwriting, trading, financial advisory and asset management. Investment banks do well when the stock market and M&A activity are strong.

Online Banks

Digital disruptors like Ally Financial Inc. NYSE: ALLY and Discover Financial Services NYSE: DFS have found their niche serving tech-savvy customers. Without expensive overhead from physical branches, online banks offer higher savings rates and lower fees.

Their stocks soared during the pandemic as digital banking gained traction. But thinning margins as rates have risen could squeeze profits going forward.

Cryptocurrency Banks

The latest entrants are crypto-focused banks like Silvergate Capital Corp. NYSE: SI. They provide banking services to cryptocurrency exchanges and investors. The extreme volatility of crypto assets makes these stocks a high-risk, high-reward venture.

Advantages and Risks of Investing in Bank Stocks

Investing in bank stocks can offer several potential benefits for investors seeking exposure to the financial sector. But there are always risks, too. Let’s explore both.

Advantages

Here are some of the key advantages:

- Potential for dividend income: Many major banks pay regular dividends to their shareholders. Dividend yields for bank stocks are often higher than average, providing a steady stream of income. Larger, more established banks tend to have higher dividend payouts.

- Historical stability and long-term growth: Bank stocks tend to be less volatile than the overall market. They provide stability amid economic ups and downs, especially if you’re a conservative investor looking for long-term growth potential.

- Diversification opportunities: Investing in bank stocks allows you to diversify your portfolio across different sectors and industries. By including banks in your investment mix, you can spread risk and potentially increase returns by tapping into the financial sector’s growth.

- Exposure to financial sector trends: Banks are at the forefront of economic activity, and investing in bank stocks can give you valuable insights into broader sector trends and opportunities.

Risks

While bank stocks offer potential growth, they also come with risks to consider.

- Credit risk: Poor lending practices can lead to loan defaults and losses. Major losses from bad loans were a hallmark of the 2008 financial crisis. While lending standards have tightened, economic downturns can still lead to increased defaults and bank losses.

- Interest rate risk: A rising rate environment can boost profitability for banks as they can charge higher interest on loans. However, if interest rates rise too high, banks with large bond holdings may see the value of those assets decline. Bank profits may also fall as borrowing costs increase and loan demand decreases. Conversely, lower interest rates can squeeze margins.

- Regulatory risk: New regulations imposed on banks after the financial crisis have squeezed profits. While regulation is aimed at preventing another crisis, it does make the banking business more challenging. Banks now face more stringent capital requirements, lending limits and reporting standards, all of which can impact profitability and stock performance. Adapting to these changes and requirements is a constant challenge for management.

- Economic downturns and financial crises: Economic strife can lead to increased loan defaults and decreased profitability for banks. In times of economic uncertainty, some banks may struggle to maintain their balance sheets and could face liquidity issues. The interconnected nature of the financial system means that a crisis in one area can quickly spread to others, causing widespread panic among investors and depositors alike.

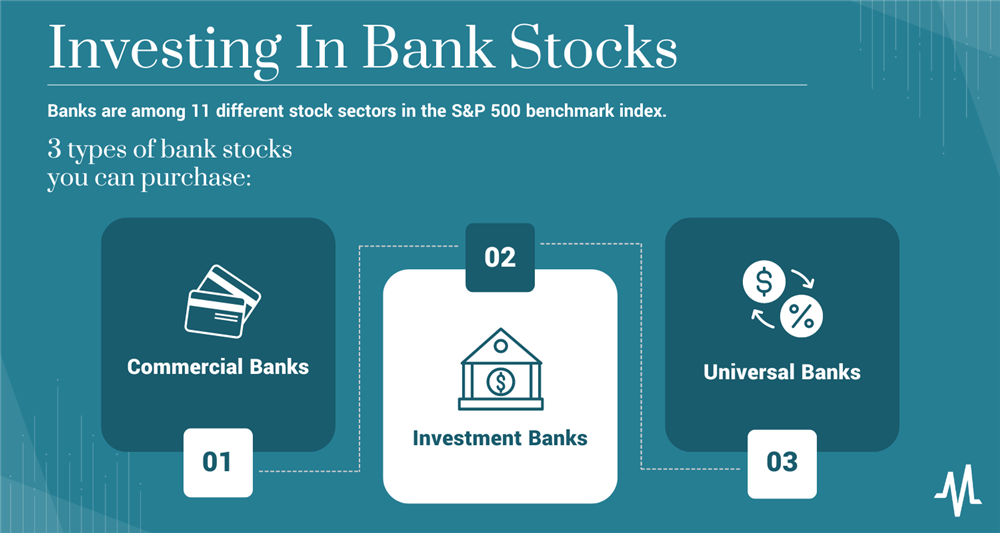

Types of Bank Stocks

Banks are among 11 different stock sectors in the S&P 500 benchmark index. While the core business model of banks is relatively easy to understand because they take customer deposits and make loans, different types of banks specialize in other areas.

Banks have expanded to include more financial products and services beyond providing loans, checking and savings accounts. Banks must have a federal and/or state charter to conduct banking services, which also provides Federal Deposit Insurance Corporation (FDIC) coverage for deposits up to $250,000 per account. The FDIC does not cover investments.

Commercial Banks

Commercial banks are the most recognized types of banks that fit the traditional operating model of taking deposits, providing checking and savings accounts and lending services to retail and business customers. They provide personal to commercial loans, from credit cards and mortgages to working capital for your business. The federal government charters these national banks, which are members of the Federal Reserve System.

Investment Banks

These banks provide financial services like raising capital, introducing high-net-worth investors, debt and structured financial product offerings, underwriting IPOs, advising and facilitating mergers and acquisitions and other complex financial transactions to corporations and governments. They tend to have higher net-worth clients for their wealth management, asset management and advisory services in addition to providing private banking functions.

Universal Banks

These banks are a one-stop-shop providing services found in both commercial and investment banks. From providing rewards and cash-back credit cards, investment advisory and brokerage services, and mortgage, auto, college and refi loans to CDs and money market accounts. They tend to be the largest banks by assets with the most branches and ATM networks, often called money center banks, serving consumers and businesses nationally.

How to Value and Buy Bank Stocks

To analyze and quantitatively value a bank stock, you should use its latest earnings report data to apply specific standard financial metrics for profitability. Disregard book value and cash per share when it comes to analyzing bank stocks, as most screeners apply customer funds into the equation, which distorts the value and is technically not owned by the bank. Book value also considers intangibles, including brand names, patents and goodwill, which is subjective or easily inflated.

Step 1: Calculate the net interest margin (NIM).

This ratio is how much the bank makes on the interest it charges on loans minus the interest it pays out on savings accounts. Rising interest rates bump up this metric since it enables the bank to charge more for its loans. You can derive it by calculating net interest divided by total interest-generating assets multiplied by 100. A 3% margin or greater is attractive.

Step 2: Calculate the return on equity (ROE).

This ratio measures the profits as a percentage of shareholders' equity. In other words, how much would be left over to be returned to shareholders if the bank paid off all its debt and sold its assets? You can calculate this by dividing net income by total shareholder's equity times 100. A result greater than 10% is an attractive baseline.

Step 3: Calculate the return on assets (ROA).

The return on assets (ROA) ratio is the percentage of net income relative to its total assets, including cash, cash equivalents, securities, interest-bearing loans, property, etc. You can calculate it by dividing net income by total assets, multiplied by 100. A greater than 1% figure is attractive.

Step 4: Calculate the efficiency ratio (ER).

As the name implies, this ratio measures the efficiency of a bank's operations based on how much of its top line goes toward paying operating costs. You can calculate it by dividing noninterest expenses by net revenues times 100. An efficiency ratio under 60% is desirable.

Step 5: Calculate the price-to-earnings (P/E) ratio.

This ratio helps compare the valuation of stock to its industry peers. You can calculate it by dividing the stock's last trade price by its earnings per share (EPS). It's what an investor would pay for every $1 of profit, assuming the company will generate profits.

Companies that don't generate profits don't have a P/E ratio. You can use the P/E ratio of a specific bank to compare against the industry average or other peer banks. You can compare it to historical P/Es for the particular bank or industry to see if the bank stock is relatively cheap compared to peers. You can use it in comparison to benchmark indices like the S&P 500 and find undervalued stocks. For example, if the industry average P/E for commercial banking is a 10 and you see a bank stock for six, it may be considered undervalued.

Ways to Buy Bank Stocks

There are many ways to buy bank stocks based on your risk profile, but how to buy bank stocks? A simple purchase through a registered online broker does the trick if you have researched and prepared for the highest-risk option to buy a specific bank stock — it can help you buy bank stocks quickly and efficiently.

However, if you want to spread your risk by investing in a broader number of bank stocks, you can purchase a mutual fund. If you prefer the diversification of a mutual fund combined with the execution of a trading stock, consider buying an exchange-traded fund (ETF) which can contain many different finance stocks. ETFs trade like stocks but track indexes like mutual funds — they are more liquid.

You can take a general S&P 500 financial sector ETF or invest in specific types of bank stocks or themes. The more liquid ETFs tend to include stocks widely traded and/or those that are components of major benchmark indices like the S&P 500 or Dow Jones Industrial Average.

How to Assess a Bank's Risk

You may think that banks are consistently profitable, low-risk investments, but that's not always the case. Banks are leveraged businesses. There are definite risks involved when investing with banks. To provide loans, banks leverage the money they take in. Banks try to hedge their risk as leverage grows.

It can become a game of Jenga, where a collapse in one business area can disrupt the whole operation. If banks lose too much money on leverage, they can become insolvent, as became terrifyingly apparent during the 2008 financial crisis. Since then, safeguards have been put in place by the Federal Reserve and Treasury Department to ensure banks are well-capitalized and run periodic stress tests under stringent capital requirements. You can also assess a bank's risk by watching two critical risk metrics based on lending practices: the nonperforming loan ratio and net charge-offs.

The nonperforming loan (NPL) ratio measures the percentage of nonperforming loans divided by the total amount of the bank's outstanding loans. Nonperforming loans at least 90 days delinquent on payments are subsequently at risk of default. The lower the NPL percentage, the better. Ideally, under 2% is attractive.

Net charge-offs (NCOs) are loans the bank can't completely recoup, as the borrower can't or won't pay back the debt. The bank loses on that loan, which becomes an uncollectable debt after six months of non-payment. The net charge-off is the dollar amount of the loan which the bank can't recoup or the gross loan amount minus any subsequent recovery of the delinquent debt, such as collections.

This is especially relevant with unsecured debt like credit cards versus secured loans like mortgages and auto loans. The NCO ratio is the annualized ratio of net charge-offs divided by the average outstanding loans times 100 and tracked by the Federal Reserve. Investors can track the history of net charge-off ratios, as a rising percentage can be a warning sign. For example, if a commercial bank had a net charge-off percentage of 2.41% in 2021 and rises to 2.61% in 2022, it's a 20-basis point jump, signaling weakening economic conditions and/or lax credit standards for the bank. An NCO rate of less than 1.5% is an ideal benchmark.

Bank Stock Dividends

Most banks pay stock dividends. There are extreme situations where they may cut or halt dividend payouts during a credit crisis, economic downturns and periods of losses. However, bank dividends tend to be stable, which makes them attractive income-generating investments. The annual percentage yield can fluctuate based on the underlying stock price.

Therefore, a high dividend may not compensate for the loss absorbed by the decline in the stock price if you are an investor. Dividends often provide a cushion of safety for the underlying stock price volatility but can be irrelevant if the stock falls more than the annual dividend yield.

Key Metrics for Evaluating Bank Stocks

Here are some key metrics to consider when evaluating bank stocks:

Price-to-Earnings (P/E) Ratio

The price-to-earnings (P/E) ratio is one of the most widely used valuation metrics for stocks, including banks. It measures a company's current share price relative to its earnings per share (EPS) and provides insight into how much investors are willing to pay for each dollar of the company's earnings.

A lower P/E ratio generally indicates the stock is undervalued, while a higher ratio suggests overvaluation.

Price-to-Book (P/B) Ratio

The price-to-book ratio compares a company's market capitalization to its book value. The ratio provides insight into whether a stock is undervalued or overvalued by analyzing the company's market price in relation to its underlying assets.

A lower P/B ratio tends to indicate a stock is undervalued, while a higher ratio might mean overvaluation. The P/B ratio is calculated by dividing the company's current market price per share by its book value per share. This book value is determined by subtracting the bank's liabilities from its total assets, then dividing this figure by the number of outstanding shares. Banks with a P/B ratio of less than 1 are often considered a bargain, as it implies that the market values the bank's assets less than their accounting value.

Return on Equity (ROE) and Return on Assets (ROA)

Return on assets (ROA) and return on equity (ROE) are profitability metrics that evaluate a bank's efficiency in generating profits from its assets and shareholders' equity, respectively.

ROE measures how efficiently a bank generates profits from shareholder equity. Look for banks with an ROE consistently above 10%. Return on assets (ROA) gauges how well a bank uses its assets to generate profits. It’s calculated by dividing net income by average total assets. A higher ROA indicates greater profitability and efficiency in using assets to generate income. An ROA above 1% is considered solid.

Net Interest Margin (NIM)

This reveals the profitability of a bank's lending practices and shows the difference between interest income generated and interest paid out. A wider margin indicates higher profitability. Over 3% is considered a good NIM.

High-quality loans mean that borrowers are making timely payments, and there’s a low risk of default. But lower quality loans indicate a higher risk of defaults and charge-offs, which could potentially result in losses for the bank.

Non-performing loans (NPLs) deserve special attention as those are outstanding loans in which the borrower has not made the scheduled principal or interest payments for a specified period. These are generally considered “bad debts,” posing a significant risk to a bank's stability and efficiency.

The NPL ratio, which is the total amount of nonperforming loans divided by the total amount of outstanding loans, offers a clear snapshot of the bank's loan portfolio quality. The higher the NPL ratio, the greater the risk to the bank's stability. Typically, a bank with an NPL ratio of less than 1% is considered healthy.

Strategies for Investing in Bank Stocks

Investing in bank stocks calls for a blend of robust strategies including diversification, analysis of financial statements, a keen eye for regulatory changes and industry trends, strategic dollar-cost averaging and careful consideration of dividend reinvestment plans (DRIPs).

Diversification Across Different Types of Banks

You can maximize your risk-adjusted returns by diversifying your portfolio across various types of banks including commercial banks, investment banks, regional banks, savings and loans institutions and credit unions. Each type has its unique strengths, weaknesses and business models. For instance, commercial banks often offer a steady stream of income through their loan and deposit services, while investment banking can generate large profits, albeit with higher risks, through their trading and investment activities.

Regional banks, though smaller, often have strong ties to local communities, which can provide stability during economic downturns. Savings and loans typically focus on mortgages and other consumer loans, providing you a steady flow of income. Credit unions, being cooperatives owned by members, usually boast high customer satisfaction rates and often have competitive rates on loans and savings accounts.

Financial Statement Analysis

Analysis of a bank’s financial statement involves looking at its income statement, balance sheet and cash flow statement for indicators of financial health.

The income statement provides information about a bank's revenues, expenses and profits over a particular period. Look out for consistent growth in net interest income, which is the difference between interest received from loans and interest paid on deposits. Also, scrutinize non-interest income sources like fees and charges as these can significantly bolster the bank's revenue.

The balance sheet reflects a bank's assets, liabilities and shareholders' equity at a specific point in time. It provides insight into the bank's capital adequacy and liquidity. Key indicators to look out for include the bank's loan-to-deposit ratio, which can signal the bank's liquidity risk, and its reserve ratio, a measure of how well the bank is prepared to handle loan losses.

The cash flow statement, on the other hand, reveals how much cash is coming into or leaving a bank during a certain period. The ability of a bank to generate strong operating cash flows is a positive sign of its financial stability and profitability. Pay close attention to the bank's cash flow from operations and from investing and financing activities.

Keeping an Eye on Regulation

Banking is a heavily regulated industry, and any change in regulations can impact a bank's profitability. Be sure to stay updated on regulatory changes and understand their implications for your bank stocks.

Following industry trends like technological advancements, shifts in consumer behavior or macroeconomic factors can give you an edge in finding potential winners or losers in the banking sector. For instance, the trend towards digital banking has been a game-changer for many banks, allowing them to serve customers better and with lower overhead. But banks that have been slow to adapt to this trend have lost market share.

Strategic Dollar-Cost Averaging

This involves investing a fixed dollar amount in bank stocks at regular intervals, regardless of the share price. Thus you buy more shares when prices are low and fewer shares when prices are high, potentially reducing your overall cost per share over time. It’s a good strategy for mitigating risk, especially during volatility in the stock markets.

Dividend Reinvestment Plans (DRIPs)

Many banks offer DRIPs, which allow shareholders to reinvest their cash dividends back into additional shares or fractional shares. This can be a powerful compounding strategy over the long term, as it enables you to increase your holding in high-quality bank stocks without having to spend more money.

On the flip side, remember that DRIPs may not be suitable for everyone. If you rely on dividends for income, then automatically reinvesting these dividends may not be the right approach for you.

How to Assess a Bank’s Risk

If you want to make informed decisions, risk assessment is key. For example, say you’re thinking of investing in a traditional, established bank that provides personal accounts, business accounts, mortgages, loans and investments. On the surface, it seems like a rock-solid institution. But how can we assess its risk?

First, we’ll look at the bank's capital adequacy. This is essentially the financial cushion available for the bank to weather losses without becoming insolvent and protects depositors in case of a downturn. The bank's capital-to-assets ratio is a good indicator of its capital adequacy. A high ratio signifies that the bank has a strong buffer against losses.

Next, consider the bank's credit risk: the potential that borrowers will default on their loans. Look at the bank's non-performing loans (NPL) ratio; a lower ratio is better since it implies that most of the bank's loans are being repaid.

Also assess market risk, which is the risk that changes in market prices and rates will negatively impact the bank's assets or liabilities. For instance, if interest rates rise, banks may have difficulty attracting borrowers, which could decrease their profitability. To gauge this, keep an eye on the bank's interest rate risk management and observe how they adapt to changes in the market.

The fourth area is operational risk: the potential for losses from inadequate or failed internal processes, people and systems or from external events. This could include anything from cyber-attacks to natural disasters. The bank's disaster recovery plans and cybersecurity measures can give you an idea of how well-prepared it is to handle these risks.

Relying on Independent Ratings

Several independent agencies rate banks based on their financial health and stability. These ratings objectively evaluate a bank's creditworthiness and can be useful when comparing banks. These agencies, such as Standard & Poor's (S&P), Moody's and Fitch Ratings, analyze various factors like the bank's capital adequacy, asset quality, management quality, earnings predictability and liquidity.

Tips for Maximizing Returns

To navigate the jungle of bank stock investment, set realistic investment goals. Make SMART goals: specific, measurable, achievable, realistic and time-bound.

Remember to monitor your investment portfolio regularly. Market forces are dynamic, and the financial health of your chosen banks may change over time. When you regularly review your investments, you can make necessary adjustments before minor issues become major problems.

Taking a long-term perspective is key. The stock market may fluctuate in the short term, but historically, it has tended to rise over the long term. Patience and sticking to your investment strategy can yield better results than trying to time the market or reacting rashly to temporary dips.

However, investing in bank stocks — like any investment — carries its own set of risks and complexities. If you're not sure about any aspect of investing, don't hesitate to seek professional advice. Whether you rely on a financial advisor or broker, their expertise can provide valuable insights into the market and help you make good decisions. Always remember that there is no one-size-fits-all strategy when it comes to investing; what works for one person may not work for another.

Monetary Policy Impact on Bank Stocks

Banks benefit from net interest income from consumer deposits during monetary tightening periods when the U.S. Federal Reserve (the Fed) raises interest rates. However, loan demand also tends to drop. During economic expansion periods when the Fed cuts interest rates, banks make less on interest income but provide more loans as consumers take advantage of lower interest rates to finance or refinance large purchases.

FAQs

Here are some common questions you might ask when investing in bank stocks.

Are bank stocks a good investment?

Are bank stocks a good buy? Bank stocks can be a good investment during economic growth periods, so you want to find the best banks to invest in stocks. A strong economy means more loans to provide and fewer defaults, despite making less net interest income. They can buffer their earnings with net interest margin growth in economic downturns as loan volumes decline. Investment banks tend to have more IPOs, and M&A deals boost the bottom line.

What are the benefits of buying bank shares?

Bank stocks provide a dividend and potential price appreciation. They are some high-dividend stocks for those who like receiving investment income. They are generally stable investments, more so during solid economic periods than weak ones. Instead of hating on the ongoing bank fees, you can appreciate them as shareholders benefitting from their contribution to the bottom line. Also, they are not as volatile with high betas, like the FAANG stocks.

How do you choose bank stocks?

How do you know which bank stocks to buy? You can choose which bank stock(s) to invest in by fundamentally analyzing them using the above profitability, valuation metrics, and technical analysis. The technical analysis involved reviewing the underlying stock price history, trends and price patterns to gauge support and resistance price levels to gauge entry and exit points.

Before you consider Ally Financial, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Ally Financial wasn't on the list.

While Ally Financial currently has a "Hold" rating among analysts, top-rated analysts believe these five stocks are better buys.