Kemper NYSE: KMPR,

Kemper NYSE: KMPR, a provider of property, casualty, life, and health insurance in the United States is sitting near 2020 highs with earnings set to be released on Monday.

The pandemic has led to a few challenges for Kemper, but all in all, the business has held up nicely.

Is it worth getting in ahead of earnings?

Growth in Q1 2020

Kemper’s top-line growth was strong in Q1 despite pandemic-related headwinds showing up late in the quarter. Earned premiums increased 9% yoy, similar to 2019 growth rates.

While net income was just $64 million, down significantly from the $155 million reported in the prior year, that was largely due to a mark-down in equity and convertible securities fair value. Adjusted consolidated net income, which strips out that mark-down, increased 5% yoy to around $163 million.

Now let’s turn our attention to Kemper’s three segments: Specialty Property & Casualty Insurance, Preferred Property & Casualty Insurance, and Life & Health Insurance.

Solid Results Across Segments

Kemper’s Specialty segment had a strong quarter with net-earned premiums increasing 13% yoy to $823 million. The growth rate slowed in March due to the onset of the pandemic, so the segment was actually on pace to record even higher growth. In the earnings call, Kemper noted that the Florida market has outperformed with 23% growth over the trailing 12 months, partially due to the exit of a competitor.

The company’s Preferred segment saw income increase to $18 million in Q1, up substantially over the $3 million reported in Q1 2019. This was largely due to operational improvements in Kemper’s auto and home books, resulting in lower overall loss activity.

In the Life & Health segment, earned premiums increased by 2% yoy. Pre-tax income of $27 million reflected volatility in the financial markets and a couple of one-time items.

Stay-at-home orders took a lot of people off the roads, impacting Kemper’s auto insurance business. But even though auto accident frequency decreased, the severity of those accidents increased. This may be due to less traffic making it more possible for people to speed and drive recklessly. Furthermore, Kemper gave a 15% premium credit to auto policyholders in April and May to reflect the fewer miles driven.

Kemper does see a lot of potential for long-term growth in its auto segment due to fragmented competition across the country. But the current environment is presenting challenges for business.

A Strong Balance Sheet

On the Q1 earnings call, CFO James J. McKinney spoke about Kemper’s financial position:

“I would like to start by reviewing some of the key financial data points that highlight the strength of our balance sheet. First, we have over $871 million in liquidity, many multiples of our fixed costs. Second, our diversified model is designed to produce positive cash flow through volatile economic periods. In the quarter, operating cash flow was $62 million. A final item is our attractive capital stack. It is highlighted by strong capitalization of our insurance entities, a debt-to-capital ratio of 17% and no near-term debt maturities.”

Excellent Valuation & Impressive Long-Term Growth

Kemper is trading at between 12 and 13x projected earnings for both 2020 and 2021.

On top of that, Kemper’s revenue and net income have been trending upwards for years. Over the past five years, revenue has grown at a CAGR of 18% and net income has grown at a CAGR of 36%.

While Kemper is unlikely to see revenue or net income grow at a CAGR in the double-digits over the next five years, shares would quickly become a stellar value even if growth ends up in the mid-single-digits over the next five years.

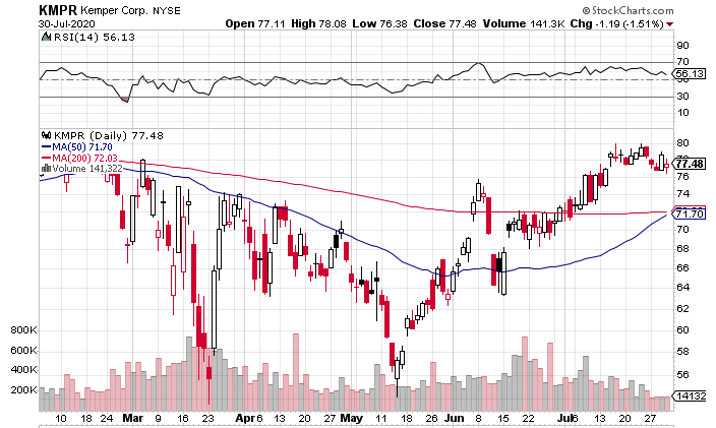

How Does the Chart Look?

Kemper has spent the first seven months of 2020 in a base between around $53 and $81 a share. Shares are currently sitting near the top of that range ahead of earnings.

Volume has been extremely light this week, showing that investors are holding their shares following the recent move to the top of the range. The 50-day moving average should cross over the 200-day moving average in the next couple of sessions, which would offer a technical tailwind for KMPR.

While Kemper is trading at a very reasonable valuation, I think it’s best to wait for a decisive breakout above $82 a share, perhaps on earnings. $82 a share is less than 6% above current levels, meaning that waiting on a breakout won’t cost you much.

The confirmation that a breakout would provide is worth paying a few bucks more.

The Final Word

Even though Kemper shares are very appealing at these levels, it’s best to wait for a breakout to get in – which likely means waiting until after earnings are announced.

The good news is that even after a great report, shares should have plenty of more room to run.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

MarketBeat just released its list of the 7 hottest IPOs expected to hit Wall Street in 2026. See which companies are preparing to go public and why investors are watching closely.

Get This Free Report