I love stocks that stage explosive breakouts.

The type of breakouts where a stock moves 8%+ higher on big volume, zooming past resistance.

But if there’s a downside to that type of price action, it’s that it can be difficult to find a logical place to put your stop order. You often have to draw an arbitrary line in the sand, or place your stop more than 10% below your entry point.

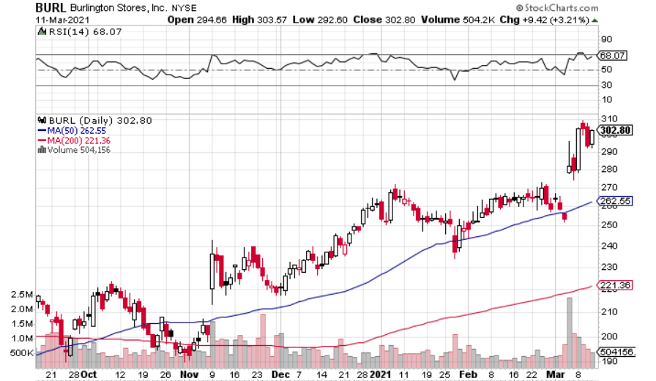

Burlington NYSE: BURL has not recently staged an explosive breakout – but it is showing signs of an emerging uptrend and presenting an attractive entry point with clear (and near) places to put your stop-order.

Why does this look like an emerging uptrend?

Burlington is coming off of two short-term bases (the blue and red boxes), culminating in mini-breakouts. Now, shares have pulled back to near the latest breakout point, putting in a reversal at the 200-day moving average.

If you get in at Friday’s close, and place your stop-order just below the 200-day moving average, you would have a downside of less than 2%. Move that stop-order to just below the 50-day moving average, and your downside is still less than 6%.

Burlington Posted a Loss in Q2

In Q2, Burlington lost 56 cents per share, on an adjusted basis, with revenue that was down 39% yoy to $1.01 billion. The revenue fell short of analyst estimates of $1.13 billion, but the adjusted EPS came in well-above expectations, which called for a loss of $1.06 a share.

There is a lot of uncertainty in the near future, and Burlington acknowledged as much by not issuing guidance for the rest of the year.

CEO Michael Sullivan flat-out said that the off-price retailer has “a lot of risk in Q3.”

It’s Not All Bad for Burlington

Dig into the Burlington numbers and you’ll see several reasons for optimism:

- Burlington did not show traditional comps, but it did calculate its sales in re-opened stores. Those fell 14% from the time they re-opened to the end of the quarter, compared to the year-ago period. Still not too good, but much better than down 39%.

- Gross margins were 45.9% of sales, much better than 39.2% consensus estimates and up from 41.6% in the year-ago quarter. Burlington discounted its products less than many of its peers, which contributed to the expansion.

- Burlington’s inventory is down 26.2% from a year ago. On the Q2 earnings call, management noted that there was a lot of pent up demand when stores re-opened in June, with sales trending higher month-by-month.

On that last point, part of the reason for Burlington’s huge revenue decrease was a lack of inventory. Burlington has managed its business conservatively since the onset of the pandemic, but demand is higher than expected.

Burlington will replenish its inventory to meet demand, particularly as struggling full-priced stores look to downsize.

Couple that with store-openings and you have a recipe for improving comps over the remainder of 2020.

And Burlington is actually set to expand its footprint this year, with the company looking to open 62 new stores in 2020, compared with 26 closed or relocated stores.

Long-Term Outlook is Bright

Over the past five years, prior to the onset of the pandemic, Burlington was consistently recording revenue growth in the high-single-digits to low-double-digits. It would take a minor miracle for Burlington to see revenue growth in Q3 or Q4 2020, but post-pandemic, I expect Burlington to pick up where it left off.

Most analysts agree. While 2021 will have easy yoy comps, Burlington is expected to see more than 10% revenue growth in 2022.

Burlington is trading at 29.2x projected 2021 earnings and 23.5x projected 2022 earnings, so earnings growth is expected to outpace revenue growth. The company’s margin expansion in a tough business climate bodes well for the future.

And Burlington has less than 800 stores – all in the U.S. – so it still has plenty of room for expansion.

The Verdict

Burlington has the ability to make its current share price look very cheap in a few years.

There are a few “ifs” in the analysis, but the ceiling is too high to pass this one up.

Add in the attractive entry point with the limited downside, and you should seriously consider picking up some Burlington shares.

Before you consider Burlington Stores, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Burlington Stores wasn't on the list.

While Burlington Stores currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

MarketBeat's analysts have just released their top five short plays for June 2026. Learn which stocks have the most short interest and how to trade them. Click the link to see which companies made the list.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.