Key Points

- NXP Semiconductors had a solid quarter in which its diversified offerings helped sustain stable cash flows.

- The guidance includes a return to growth that should be sustained into 2024.

- Trading at 13.5X earnings and paying 2.25%, it is a healthy and attractive yield among chip and tech stocks.

- 5 stocks we like better than NXP Semiconductors

The microchip market is suffering from lingering issues, but signals in NXP Semiconductors NASDAQ: NXPI Q3 report suggest the bottom is in for this stock if not the broader market. While there were weaknesses within the report, the big picture is that stabilization is at hand, and growth is back on the table.

Assuming that resilience can carry into 2024, this company will continue to improve its guidance and lead the market higher. Until then, it presents a high-yield value to investors seeking exposure to tech, microchips, and the applications of AI.

NXP Semiconductors beats and raises after a turbulent quarter

NXP Semiconductors had a solid quarter despite slowing in some segments and weakness in others. The company produced $3.43 billion in net revenue for a decline of 0.6% YOY but outpaced the consensus by nearly an entire percentage point.

The top-line resilience is due to outperformance in Mobile and IoT/Industrial, which both contracted compared to last year and by strength in the Automotive segment, which posted a gain of 5%. Communications and Other grew by 8% but came in slightly weaker than forecast. The takeaway is the diversified business model is aiding the recovery, and guidance includes a return to growth.

The margin news is also favorable to shareholders. The gross margin expanded, the operating margin contracted, and the net income margin was relatively flat to leave adjusted earnings at $3.70. This is up $0.16 compared to last year and outpaced the Marketbeat.com consensus by a dime, strengthening the outlook for next year and the company’s financial health.

The guidance is also supportive of the market. The guidance was raised at the top and bottom line to a range bracketing the consensus figures. While the figures include margin compression and a chance for YOY contraction, the takeaway is that Q4 results will probably be flat to slightly higher and cash flows are sufficient to sustain the capital return outlook.

NXP Semiconductors offers yield with value among tech stocks

NXP Semiconductors pays a solid and healthy dividend compared to most tech stocks. The payout runs near 2.25%, with shares trading near critical support, and the distribution comes with a fortress balance sheet to protect it and a growth outlook. The payout is less than 30% of the earnings guidance and consensus EPS target for next year, and there is a growth history.

The distribution is compounded by share repurchases, which more than double the effective yield. Share repurchases are offset by share-based compensation expense but only partially. Net of share-based compensation, repurchases were more than $200 million in Q3 and are expected to continue.

The company’s FCF is sufficient to pay the distribution, raise it as expected, and continue repurchasing shares while it invests in business and builds capital. Balance sheet details include an increase in cash, current assets, total assets, and equity compounded by a reduction in long-term debt. Leverage remains low at 2.1X total and 1.3X net.

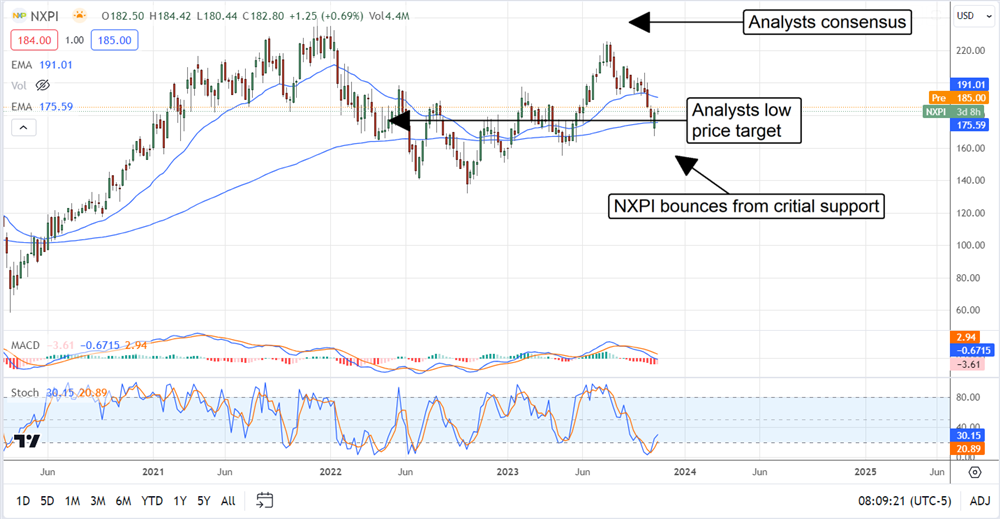

NXP Semiconductors trades at the analysts' floor

The price action in NXPI has been under pressure since June, but a floor is in. The technical action is bottoming near the 150-week EMA, consistent with the lowest analyst price target tracked by Marketbeat. The floor in action is compounded by the solid green candle confirming support at the EMA and the indicators, which are set up for a bullish swing within an upwardly biased trading range. In this scenario, the market could quickly move up to the analysts' consensus target of $228, a gain of 25%.

Before you consider NXP Semiconductors, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and NXP Semiconductors wasn't on the list.

While NXP Semiconductors currently has a "Moderate Buy" rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

As the AI market heats up, investors who have a vision for artificial intelligence have the potential to see real returns. Learn about the industry as a whole as well as seven companies that are getting work done with the power of AI.

Get This Free Report